Understanding Cash to Close in Real Estate

Navigating the real estate market can be complex, especially when it comes to understanding the various financial terms involved. The journey to homeownership is often fraught with legal jargon and financial nuances that can overwhelm both first-time homebuyers and seasoned investors alike. One such term that often confuses many is "cash to close." This article aims to demystify cash to close by breaking down its meaning, its components, and how it differs from other related terms. By understanding these concepts, buyers can approach the closing table with confidence and a clear grasp of their financial commitments.

Signed Contract

Cash to close refers to the total amount of money a buyer needs to bring to the closing table to finalize a real estate transaction. This figure is a culmination of various expenses that ensure the buyer has sufficient funds to complete the purchase of the property. While often misunderstood, cash to close is a critical part of the home buying process that goes beyond just the down payment. It encompasses several other costs associated with the transaction, and failing to understand it fully can lead to financial shortfalls or delays in the closing process.

The cash to close amount is typically outlined in the closing disclosure form provided by the lender a few days before closing. This form is crucial as it provides a detailed breakdown of the costs and fees involved. Being aware of this information not only prepares the buyer financially but also helps in verifying the accuracy of the charges, ensuring there are no discrepancies that could affect the transaction.

Components of Cash to Close

Understanding the components that make up the cash to close is essential for any buyer. Each component plays a specific role in the transaction process, and knowing what each entails can prevent unexpected expenses.

1. Down Payment: This is the initial amount you pay toward the purchase price of the home. It is a significant part of the cash to close but not the entirety of it. The down payment represents your equity in the property and is usually a percentage of the home's purchase price, often ranging from 3% to 20% depending on the loan type and lender requirements.

2. Closing Costs: These are fees and expenses associated with finalizing the real estate transaction. They can include appraisal fees, title insurance, attorney fees, and more. It's important to note that closing costs can vary based on the location and the specifics of the transaction. For instance, certain states may have additional fees, and the complexity of the transaction can also influence the cost.

3. Prepaid Expenses: These are costs that cover future expenses related to the property, such as homeowner's insurance and property taxes. These funds are typically placed in an escrow account. Prepaid expenses ensure that certain property-related bills are paid in advance, which protects both the lender and the buyer from future financial surprises.

4. Escrow Funds: In some cases, lenders require buyers to set aside funds in an escrow account to cover property taxes and insurance for the first year. This requirement provides assurance to the lender that these essential expenses will be managed appropriately, safeguarding their investment in the property.

Estimated Cash to Close

The estimated cash to close is an initial calculation provided during the mortgage application process. This estimate gives buyers a rough idea of how much they will need to bring to the closing table. However, it is important to remember that this figure is subject to change as the closing date approaches and more accurate information becomes available.

Several factors can influence the estimated cash to close, including changes in the loan amount, interest rates, or additional negotiations with the seller. Buyers should remain in close contact with their lender and real estate agent to receive updates and ensure they are financially prepared for any adjustments. By staying informed, buyers can avoid last-minute surprises and have peace of mind knowing they have the necessary funds ready for closing.

Cash to Close vs. Closing Costs

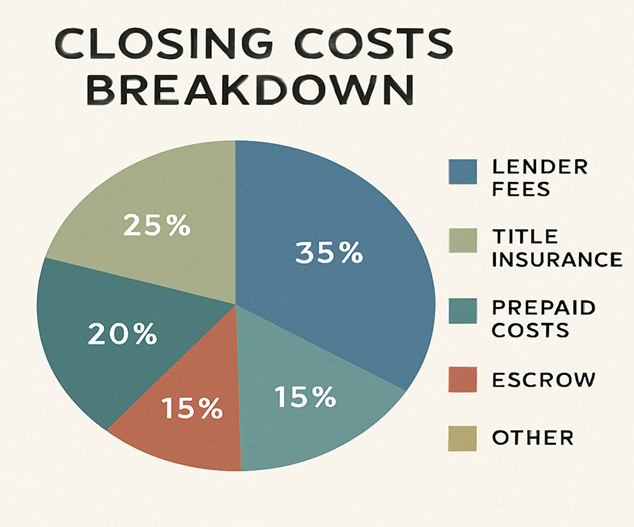

Closing cost breakdown

A common point of confusion is the difference between cash to close and closing costs. While they are related, they are not the same thing, and understanding the distinction is crucial for financial clarity during the home buying process.

● Cash to Close: As previously mentioned, this is the total amount needed to finalize the purchase. It includes the down payment, closing costs, prepaid expenses, and escrow funds. Essentially, cash to close encompasses all the funds a buyer must provide to complete the transaction and take ownership of the property.

● Closing Costs: These are part of the cash to close but only represent a portion of the total. Closing costs are fees incurred during the home buying process and can include lender fees, title fees, and other miscellaneous charges. Unlike the broader cash to close figure, closing costs specifically relate to the administrative and legal expenses required to transfer ownership of the property.

Understanding this distinction helps buyers accurately budget for their home purchase and ensures they are aware of the full scope of expenses involved. Clear communication with lenders and real estate agents can further clarify these terms and provide additional insights into potential cost-saving opportunities.

Does Cash to Close Include the Down Payment?

Yes, the cash to close includes the down payment as one of its primary components. It is essential to differentiate between the two to avoid any financial surprises at closing. The down payment is the percentage of the home's purchase price that you pay upfront, while cash to close is the total out-of-pocket expense required to complete the transaction.

Recognizing that the down payment is a part of the larger cash to close calculation allows buyers to have a more comprehensive understanding of their financial responsibilities. This awareness can help in planning and securing the necessary funds well in advance of the closing date, ensuring a smoother transaction process.

How to Calculate Your Cash to Close

Understanding how to calculate your cash to close can help you budget effectively for your home purchase. Here's a simplified process:

1. Start with the Down Payment: Determine the percentage of the home's price that you'll be paying upfront. This is a critical first step in calculating your cash to close, as it sets the foundation for your overall financial commitment.

2. Add Closing Costs: Obtain an estimate of closing costs from your lender or real estate agent. This estimate should include all expected fees and charges, providing a clearer picture of the total expenses involved.

3. Include Prepaid Expenses and Escrow Funds: These amounts can usually be provided by your lender. Understanding these components helps ensure you are accounting for future expenses that need to be paid at closing.

4. Subtract Seller Credits or Concessions: If the seller has agreed to cover some of the closing costs, subtract these from your total. This can significantly reduce the amount of cash you need to bring to closing, making the transaction more affordable.

5. Review Your Loan Estimate: Your lender will provide a loan estimate that includes a detailed breakdown of all costs, including the cash to close. Reviewing this document carefully ensures accuracy and helps you verify that all calculations align with your expectations.

Importance of Understanding Cash to Close

by Pauli Nie

by Pauli Nie (https://unsplash.com/@paulify)

Having a clear understanding of cash to close is crucial for several reasons. This knowledge not only prepares buyers financially but also enhances their overall home buying experience.

● Financial Preparedness: Knowing the exact amount you need to bring to closing helps you avoid last-minute financial stress. Being prepared financially ensures that the transaction proceeds smoothly, without unexpected obstacles.

● Avoiding Delays: Inadequate funds at closing can delay the transaction, potentially costing you the property. Ensuring you have the required cash to close ahead of time helps prevent such setbacks, keeping your homeownership goals on track.

● Better Budgeting: Understanding all components allows you to plan your finances more effectively and make informed decisions. By considering every aspect of the cash to close calculation, you can allocate resources wisely and maintain control over your financial situation.

Final Thoughts

Cash to close is a vital concept in the real estate purchasing process. It encompasses all the costs a buyer needs to cover to successfully close on a property. By understanding what cash to close includes and how it differs from closing costs, buyers can better prepare financially and avoid unexpected surprises.

Whether you're a first-time homebuyer or a seasoned investor, having a firm grasp on cash to close can make the process smoother and more transparent. Always consult with your real estate agent or financial advisor to ensure you have the most accurate and up-to-date information regarding your specific situation. Staying informed and proactive in understanding these terms can empower you to make confident decisions as you move forward in your real estate journey.

Remember, being well-informed is your best asset in navigating the complexities of real estate transactions. With the right knowledge, you can confidently take the final steps towards owning your dream home, knowing you are fully prepared for the financial obligations involved.